Facebook

Facebook Google

Google GitHub

GitHub Linkedin

LinkedinThe Cryptocurrency Mining Craze: Energy Consumption, Hardware, and the Controversies in Between

Cryptocurrency mining has become so rampant that it has had a fairly significant impact on the GPU market and even electricity theft.

Bitcoin and cryptocurrencies have brought blockchain, algorithms, GPUs, and security issues into the public consciousness. Cryptocurrency mining, however, has also introduced issues of hardware shortages and changed the way we look at currency generation. So—what's up with Bitcoin mining?

While the value of Bitcoin (and most other cryptocurrencies) decreased significantly at the beginning of 2018, there appears to be momentum again with values rising. Cryptocurrency mining has become so rampant that it has had a fairly significant impact on the GPU market, and more regularly news article are popping up about stolen electricity for the purpose of cryptomining.

Here's some basic information about cryptocurrencies (primarily Bitcoin), mining, and why it matters.

A Brief History of Bitcoin

In 2008, a white paper was released titled “Bitcoin: A Peer-to-Peer Electronic Cash System”, authored by Satoshi Nakamoto, though that name is widely understood to be a pseudonym. This white paper was one of the first widely popular uses of the term Bitcoin.

The core idea of Bitcoin was to be a form of decentralized, private currency that used the blockchain to keep a record of how currency was spent, and to use a distributed network of nodes that would all confirm, or deny, a transaction occurred. If the majority of the node network agreed that the transaction was valid, it would be added to the master blockchain and become part of the “ledger” forever. It solved double spending, decentralization, and was envisioned as the currency of the future where no government or bank controlled it. Part of the incentive of setting up and running a Bitcoin node is that there is a reward in exchange for work. So, by installing the Bitcoin software and lending your CPU/GPU to the cause, users could make virtual money.

In Bitcoin’s beginnings, it developed a reputation of being a quirky Internet currency often associated with shady purchases on the Deep Web. Some people “mined” for Bitcoin, that had a maximum value of only $0.39 in 2010. Just shy of a decade later, cryptocurrencies have exploded in popularity and created their own culture around its use. There are now countless blockchain-based projects and currencies, all with different use cases, advantages, and disadvantages. There is also an accompanying lexicon now associated with cryptocurrencies (“HODL”, “to the Moon”, etc).

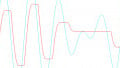

In late 2017, Bitcoin’s highest value to date peaked, reaching a value of nearly $20,000 per Bitcoin, drawing even more interest into cryptocurrencies.

Bitcoin's value peaked in lae 2017. Image courtesy of CoinMarketCap.

While the value of Bitcoin (and most other cryptocurrencies) decreased significantly at the beginning of 2018, there appears to be some momentum again with values rising. Predicting the value of Bitcoin is like trying to predict the stock market—there’s no foolproof way to know whether or not values will rise or fall. However, what is known is that cryptocurrency mining has become so rampant that it has had a fairly significant impact on the GPU market, driving up hardware prices, and has also increased reports of electricity theft for the purpose of cryptomining.

Focusing primarily on Bitcoin, here is some basic information on what it means to mine, what the current hardware requirements are, and why cryptocurrency mining has become controversial.

Hashcash and Proof-of-Work

As mentioned before, mining is the process of verifying a transaction and results in being rewarded for the work of doing so. In order to make this verification, the input of a hash function that matches given information about its output and a target range must be found—a mathematical problem that can take significant computer power to solve.

The first miner to find a suitable solution “wins” and Bitcoin (or whatever cryptocurrency is being mined) is awarded. In terms of blockchain, you are looking for the new block that is to be added to that chain based on the hashing output.

Bitcoin, in particular, uses the hashcash proof-of-work function. Hashcash was originally developed in 1997 as a way to prevent DoS attacks, anti-spam, and network abuse. For Bitcoin, Hashcash SHA256 is used twice for hashing (double hash)—this is more precautionary than necessary since a single SHA256 hash is sufficient for Bitcoin.

Hashcash is difficult to invert function. It is very easy to compute the hash output given an input value, but extremely difficult to find the input value given the output. To invert the function using a brute force method, the complexity would be O(2256).

In Bitcoin, the hashcash function has to be adjusted to make sure that proof-of-work can only be claimed once: a service string, a starting point, and a counter are also included so that each miner will start work at a different point, with different numbers, even if it is trying to verify the same information. Then, when a miner does succeed in finding a solution, the miners then move on to other problems. It’s a bit of a game of luck.

Image courtesy of Bitcoin StackExchange.

Mining is becoming more difficult because the algorithm adjusts based on how many “miners” there are on the Bitcoin network—the more miners and the more consensus that must be reached, the more difficult it becomes to solve each block.

A block should be solved every 10 minutes so to keep this rate, the difficulty must go up with more miners and down with less. This correlates strongly with the price of Bitcoin; if its value is high enough, then mining it even at high hardware and energy costs, is still offset. If the reward of solving a block is 12.5 BTC, then you could make $200,000 USD from a single successful solve. And if you want to be the first person to solve a problem, you have to be the fastest at doing so. That brings us to our next topic...

Current Bitcoin Mining Hardware Requirements

During Bitcoin's first years, mining didn’t require specialized hardware. With a reasonably decent laptop, Bitcoin software, and an active Internet connection, it was possible to mine a few coins. The minimum recommended system requirements are:

- 145 GB of ask space

- An Internet connection with an upload rate of 5GB/day and 500mb/day download rate

- At least a 1 GHZ > ARM chipset

- 1 GB RAM

- Windows 7/8/10 or Linux or Mac OSx

- Plus a one-time140GB download of Bitcoin core

Seems fairly accessible, right? There are, however, professional Bitcoin mining “farms” being established where warehouses are lined up with shelves of ASICs solving blockchain problems. When competing with setups like this, mining from a standard laptop using a CPU or GPU is becoming a fairly useless effort especially relative to the actual cost for the electricity to do so.

It’s this competition on the network to solve problems that has set the bar so high for hardware requirements to make it worth the investment. (Bear in mind, though, that there are some other cryptocurrencies that are still mineable using more basic hardware.)

One of many ASICs that can be purchased for Bitcoin mining. Image courtesy of Amazon.

ASICs for the purpose of Bitcoin mining is customized hardware made for the specific Bitcoin hash. While an ASIC is roughly 100,000x faster than a CPU, they run at about $3000 USD per ASIC. Furthermore, while mining, ASICs generate a significant amount of heat, requiring cooling, requiring even more electricity... You can see why the costs can become prohibitive quickly and why cryptocurrency farms tend to exist in areas where electricity is cheaper and the climate is cooler.

Controversies

So, of course, there are controversies associated with mining.

First, there is a matter of the energy used in cryptomining. When the world appears to be trending towards more efficient and “green” use of energy, cryptomining can appear to be the exact antithesis of that. There are estimates that the Bitcoin uses roughly 30 TWh of electricity per year, which is about the same as a medium-sized country (~population of 6 million people). However, it can be pointed out that large data centers easily use just as much, or more, energy.

The local effects can then be considered; in China, electricity is primarily generated from coal; reports are that a rise in cryptocurrency farms in Iceland could outpace the country’s electricity generation if not controlled; in some areas, the establishment of cryptocurrency farms is having an impact on the cost of electricity for local residents and businesses.

There has also been lots of talk about the “cryptocurrency bubble”, suggesting the value of cryptocurrency is a fad and sometime in the future will be worth nothing.

There is a battle of philosophies on how to use cryptocurrencies. Some people want to see it being constantly earned and spent as a currency, others say to “HODL” (a meme-ish, widespread misspelling of "hold"). Some use it like a stock, buy into a currency, and then sell it when it’s worth more, converting it back into centralized cash (FIAT).

An example of a cryptocurrency mining farm. Image courtesy of Kyiv Post.

Probably more upsetting to the non-cryptocurrency individual, someone hoping to simply enjoy a decent GPU, is the sudden scarcity of a reasonably affordable and decent video card for their next computer build. This is because crypto-miners are buying them en masse.

In fact, NVIDIA began to limit the number of units that could be purchased online, and cards were appearing online on third-party websites being sold for double their retail price.

Cryptocurrency and mining is an interesting new phenomenon with unexpected effects on economies, environments, and hardware supplies. There's no real way to be certain about what to expect next (will the trend continue, will it plateau, will it die off completely, will I ever be able to get a new graphics card for my PC...). But regardless of how uncertain the future of cryptocurrencies is, if its value is on the rise again, mining is probably here to stay.

Yeah i fully agree that bitcoin will rise and rise very hard! I waitting for it and want to try new tool for anonymous transfer bitcoin tumbler so any of my mined crypt can become bitcoin and then i trade it and have a lot of money!